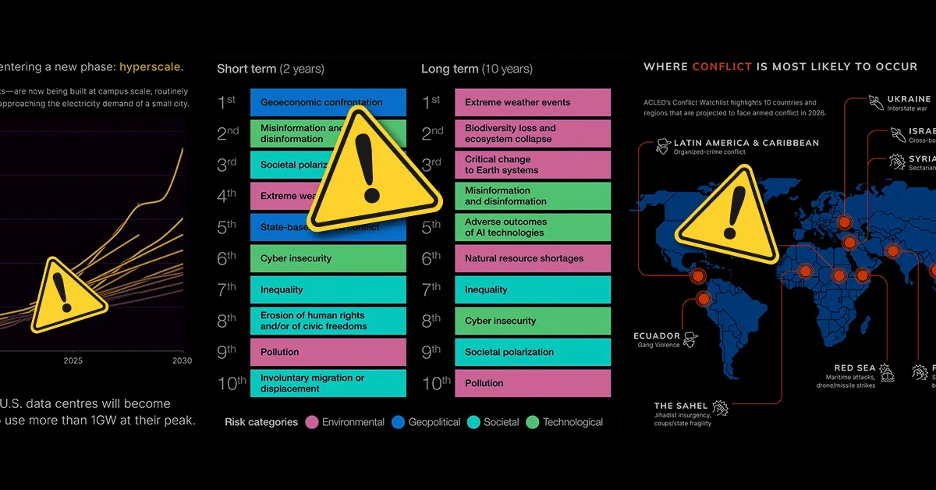

The arrival of 2026 has brought with it a level of geopolitical instability that few could have fully anticipated even twelve months ago. High-net-worth families around the globe, those managing substantial wealth across multiple continents, asset classes, and jurisdictions, are confronting a reality where traditional investment playbooks no longer suffice. The interconnected risks stemming from great-power competition, resource nationalism, alliance fractures, protracted conflicts, and sudden policy reversals have created an environment of persistent uncertainty. Leading global risk assessments, including the World Economic Forum’s Global Risks Report released in January 2026 and Eurasia Group’s annual Top Risks outlook, place geoeconomic confrontation, interstate armed conflict, and economic weaponization at the very top of concerns for the coming years.

For families whose wealth is truly international, often with origins or significant holdings outside Europe, the implications are profound. Sudden shifts in sanctions regimes can freeze assets overnight. Currency controls in one jurisdiction can ripple through global holdings. Trade barriers distort supply chains that underpin private equity investments. Regional conflicts drive commodity price spikes that fuel inflation and erode fixed-income returns. Inheritance structures meticulously built over decades can be upended by changes in bilateral tax treaties or unilateral expropriations. Privacy and discretion, cornerstone values for many affluent families, face increasing pressure from global transparency initiatives designed to counter illicit finance in a polarized world.

Yet this fragmented landscape is not without opportunity. Dislocations create entry points for sophisticated investors. Selective sanctions relief opens previously inaccessible markets. Resource contests highlight undervalued strategic assets. Independent multi-family offices, with deep expertise in more than twenty jurisdictions, proprietary algorithmic scenario modeling, and a strict fee-only alignment model, are uniquely positioned to guide clients through this terrain. They craft discreet, compliant structures that not only defend against downside risks but also position capital to benefit from the very disruptions that unsettle conventional portfolios.

This exhaustive analysis examines the defining geopolitical developments of early 2026, including the dramatic fall of Nicolás Maduro in Venezuela and the subsequent U.S.-led energy sector realignment, the constrained support Iran has received from China and Russia amid renewed nuclear tensions, and the high-profile Greenland resource and security negotiations that dominated discussions at the World Economic Forum in Davos on January 21. It then provides an in-depth exploration of broader risk themes, their specific impacts on private wealth, foundational principles for resilience, granular asset class strategies, advanced hedging techniques, family governance integration, and a comprehensive, step-by-step implementation framework.

The structural backdrop for 2026 is a decisive shift away from the post-Cold War era of deepening globalization toward a multipolar world of competing blocs. Economic policies increasingly serve national security objectives. Supply chains are “friend-shored” to allied nations. Technology ecosystems bifurcate along ideological lines. Capital flows face selective barriers. This “geoeconomic confrontation,” as the World Economic Forum terms it, ranked as the number one global risk in their January 2026 report, surpassing even climate change and cyber warfare in perceived severity over the next two years.

Early-year events have provided stark illustrations. On January 3, Venezuelan opposition forces, backed by international pressure and U.S. recognition, apprehended long-time President Nicolás Maduro. His swift extradition to face U.S. charges marked the end of an era. Within days, the Trump administration announced a series of energy agreements granting expanded licenses to American operators, notably Chevron, to resume and scale operations in the Orinoco Belt, the world’s largest proven oil reserves. Revenues are channeled through U.S.-supervised accounts, ensuring compliance with ongoing sanctions against regime holdovers. While this unlocks potentially lucrative opportunities in distressed energy infrastructure and production, it also introduces acute risks: political backlash from remaining Chavistas, legal challenges from prior expropriation claims, operational disruptions in a still-fragile security environment, and the ever-present possibility of future policy reversal if domestic U.S. politics shift.

Iran presents a contrasting case of alliance constraints. Facing renewed U.S. maximum pressure and Israeli preventive actions, Tehran has found only tepid support from its nominal partners. China continues to purchase heavily discounted Iranian crude but has refrained from provocative countermeasures, prioritizing its own economic recovery and avoidance of secondary sanctions. Russia, deeply committed in Ukraine, offers rhetorical solidarity but limited material aid. This conditional backing within the loose CRINK grouping exposes the limits of authoritarian alignment, leaving Iranian-linked investments, whether direct energy holdings or regional proxies, highly vulnerable to escalation.

The Arctic has emerged as another theater of competition. At the World Economic Forum in Davos on January 21, President Trump delivered pointed remarks on Greenland, reiterating U.S. strategic imperatives for full security cooperation and access to critical minerals essential for defense and clean energy technologies. Initial threats of tariffs on Denmark and European partners gave way to a post-summit announcement of a “framework agreement” with NATO Secretary General Mark Rutte, averting immediate trade conflict but leaving sovereignty questions unresolved. China’s existing mining interests and Russia’s northern fleet expansion add layers of complexity, turning Greenland into a microcosm of multipolar resource rivalry.

These flashpoints overlay enduring stressors: the unresolved Ukraine war sustaining elevated European energy costs and reconstruction financing needs; Middle East proxy conflicts repeatedly threatening Hormuz and Bab el-Mandeb chokepoints; U.S.-China semiconductor and AI restrictions creating parallel technological universes; and a global wave of industrial policy subsidies distorting clean energy, defense, and critical materials markets.

For private wealth, the consequences are both immediate and structural. Asset correlations spike during risk-off episodes, eroding traditional diversification benefits. Safe-haven status of certain currencies and bonds wanes under fiscal strain. Illiquid holdings in affected jurisdictions face forced sales or freezes. Multi-generational succession plans built on stable tax treaties risk disruption from renegotiations. Privacy erodes as transparency regimes expand to counter perceived geopolitical financing threats.

Historical parallels provide sobering lessons. The 1973 OPEC embargo and subsequent oil shocks triggered a decade of stagflation that devastated bond-heavy and commodity-light portfolios. The interwar period’s protectionist spiral deepened the Great Depression. Today’s environment combines these elements with modern additions: cyber vulnerabilities that can paralyze financial infrastructure in hours, sanctions regimes that reconfigure markets overnight, and information warfare that amplifies volatility through sentiment swings.

In-Depth Examination of Dominant Geopolitical Risks and Their Wealth Implications

Expanding the risk taxonomy reveals interconnected clusters.

Great-power competition between the United States and China remains the central axis. Despite occasional de-escalation signals, structural rivalry persists across trade, technology, finance, and influence spheres. Export controls on advanced nodes and AI models continue to fragment supply chains for semiconductors, electric vehicles, and renewable components. Investment screening mechanisms on both sides deter cross-border deals. Families with concentrated exposure to either ecosystem face binary outcomes: diplomatic breakthroughs could unleash rallies, while breakdowns trigger sharp corrections.

Regional armed conflicts show no signs of abatement. The Ukraine theater, now in its fourth year, sustains defense spending booms but also reconstruction financing gaps that strain European sovereign credit. Middle East escalations, particularly involving Hezbollah, Houthis, and Iranian proxies, repeatedly disrupt Red Sea shipping and threaten broader oil supply shocks.

Resource nationalism surges globally. Venezuela’s post-Maduro energy opening illustrates selective relief that benefits aligned operators while excluding others. Similar patterns emerge in lithium-rich South America, cobalt in Africa, and rare earths across multiple continents. Greenland’s mineral wealth, estimated to include substantial neodymium, praseodymium, and dysprosium deposits vital for permanent magnets, has become a focal point for U.S., Chinese, and European interests.

Alliance asymmetries expose vulnerabilities. Iran’s experience demonstrates that partnerships of convenience offer limited protection when core interests diverge. Similar dynamics play out in other groupings, affecting investment stability in aligned regions.

Hybrid and non-kinetic threats multiply unpredictability. State-sponsored cyber operations target critical infrastructure and financial networks. Disinformation campaigns amplify market swings. Selective sanctions and relief create asymmetric opportunities and traps.

The wealth impacts cascade across portfolios. Public market drawdowns occur with increasing frequency and depth. Private holdings in affected sectors face valuation markdowns or write-offs. Currency holdings in emerging or sanctioned markets suffer devaluations. Liquidity dries up as counterparties retreat. Tax and succession planning becomes more complex as treaties are renegotiated or abrogated.

Foundational Principles for Constructing Truly Resilient Portfolios

True resilience rests on evolved principles that go beyond conventional wisdom.

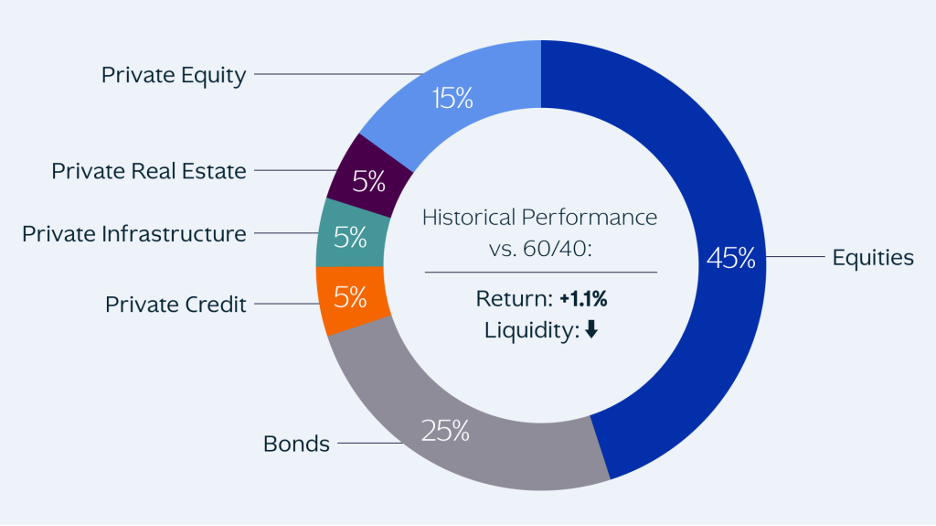

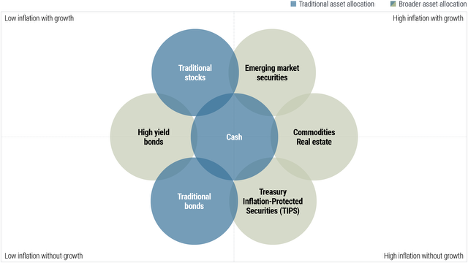

Diversification must be multidimensional: across asset classes, geographies, currencies, strategies, and time horizons. Traditional 60/40 stock-bond allocations fail when inflation and growth shocks drive positive correlations. Alternatives become indispensable for genuine decoupling.

Liquidity management adopts a tiered approach: Tier 1 immediate cash equivalents for emergencies and lifestyle continuity; Tier 2 medium-term high-quality fixed income for opportunistic deployments during dislocations; Tier 3 long-duration illiquids capturing illiquidity premiums in private markets.

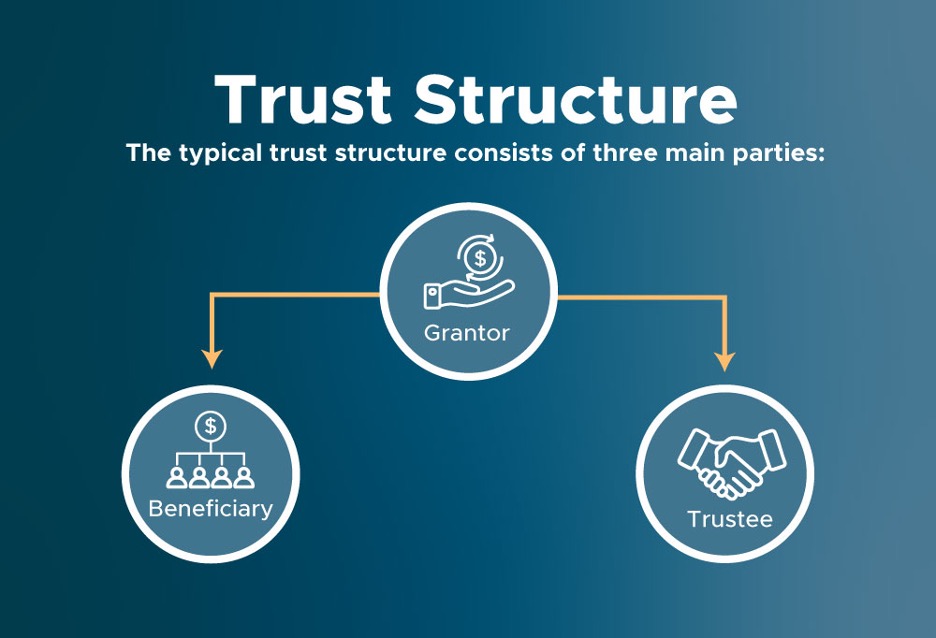

Jurisdictional diversification creates structural firewalls. Layered holding companies, trusts, and family offices across neutral, stable centers (UAE, Singapore, Cayman, Switzerland, etc.) protect against unilateral sovereign actions while optimizing tax efficiency.

Scenario-based planning, powered by proprietary algorithmic stress-testing, prepares for tail events ranging from Venezuela-style regime changes to Arctic resource conflicts or Iranian confrontations.

Family governance formalization ensures alignment across generations, embedding risk tolerances, decision protocols, and contingency plans into binding charters.

Philanthropy and sponsorship integration adds meaningful dimensions, offering tax optimization while building social legacy resilient to reputational risks.

Granular Asset Class Strategies Tailored to 2026 Realities

Public equities require rigorous selectivity. Overweight resilient themes: global defense primes and subcontractors benefiting from rearmament cycles; cybersecurity leaders addressing state-sponsored threats; essential service providers with pricing power; and commodity producers in stable jurisdictions. Underweight decoupling-sensitive sectors like consumer discretionary reliant on bifurcated supply chains.

Fixed income emphasizes quality and flexibility. Core holdings in short-to-intermediate U.S. Treasuries and select AAA sovereigns preserve liquidity and safe-haven characteristics. Inflation-linked bonds (TIPS, linkers in other currencies) counter persistent price pressures from conflicts and sanctions. High-grade corporate floaters provide yield enhancement with rate protection.

Private equity allocation focuses on non-cyclical, essential sectors: healthcare delivery and pharmaceuticals unaffected by trade barriers; regulated utilities and infrastructure with contractual cash flows; education platforms resilient to economic cycles; and waste/recycling businesses benefiting from circular economy mandates.

Private credit emerges as a standout performer in fragmented banking landscapes. Direct lending, distressed debt, and specialty finance strategies offer senior secured positions with floating rates that capture higher interest environments while providing downside protection through covenants.

Real assets deliver tangible inflation hedging and uncorrelated returns. Core infrastructure (renewable energy, transportation, data centers) features government-backed revenues and pass-through mechanisms. Farmland and timberland provide biological growth independent of financial markets. Strategic mineral royalties or production interests, carefully selected in stable jurisdictions, capture resource nationalism upside without operational exposure.

Commodities allocation adopts a strategic overlay approach: selective exposure to energy (post-Venezuela opportunities screened rigorously), industrial metals tied to defense and energy transition, and precious metals as monetary insurance.

Digital assets, for risk-tolerant families, offer non-sovereign diversification and asymmetric upside, sized conservatively within broader alternative sleeves.

Advanced Hedging Techniques and Tail-Risk Protection

Currency overlays using forwards and options neutralize unwanted forex exposures from safe-haven flows or emerging market devaluations.

Commodity futures and options programs hedge specific supply disruption risks (e.g., oil from Middle East escalations).

Systematic tail-risk strategies, long volatility, out-of-the-money put spreads, trend-following managed futures, provide convex protection against black swan events.

Dynamic rebalancing protocols exploit dislocations, deploying dry powder into oversold quality assets during panic sell-offs.

Holistic Integration of Family Governance and Next-Generation Preparedness

Resilience extends beyond financial engineering to human and structural elements. Formal family constitutions codify risk philosophies, decision hierarchies, and crisis response protocols. Regular family council meetings incorporate geopolitical briefings and scenario exercises.

Next-generation education programs emphasize financial literacy, geopolitical awareness, ethical stewardship, and philanthropic strategy. Mentorship pairings with external advisors build independent judgment.

Discreet concierge and security services address practical lifestyle risks during heightened global tensions, secure travel, asset relocation logistics, digital privacy protection.

Philanthropic vehicles, private foundations, donor-advised funds, sponsorship structures, optimize tax efficiency while creating meaningful, resilient legacies aligned with family values.

Comprehensive Step-by-Step Implementation Framework for 2026

- Full-Spectrum Exposure Audit: Conduct encrypted, algorithmic mapping of all assets, liabilities, jurisdictions, counterparties, and implicit exposures. Identify concentration risks and hidden correlations.

- Advanced Scenario Development: Model twenty-plus plausible 2026 outcomes, including Venezuela energy boom/bust cycles, Iranian confrontation paths, Arctic resource nationalizations, U.S.-China tech war escalations, and hybrid cyber events.

- Strategic Reallocation Execution: Incrementally shift portfolio weights toward resilience pillars, increase private alternatives to 40-60 percent for qualified families, tier liquidity buffers to 10-20 percent, enhance real asset exposure to 15-25 percent.

- Structural Fortification and Optimization: Design or refine multi-jurisdictional holding architectures, discretionary trusts, private trust companies, and single-family offices across optimal centers, ensuring substance compliance and tax efficiency.

- Governance and Legacy Formalization: Draft or update family constitution, establish standing risk committee, initiate next-generation education curriculum, and integrate philanthropic strategy.

- Hedging and Protection Layering: Implement currency/commodity overlays, tail-risk insurance, and dynamic rebalancing triggers.

- Continuous Monitoring and Adaptation: Deploy secure client portal for real-time visibility, quarterly algorithmic stress-testing, and immediate response capability to emerging events.

In conclusion, the intensely fragmented geopolitical reality of 2026, brought into sharp focus by Venezuela’s dramatic energy sector transformation following Maduro’s fall, Iran’s constrained support from China and Russia amid nuclear pressures, and the contentious Greenland resource and security framework emerging from Davos, presents what may be the most challenging environment for private wealth preservation in a generation. Yet for internationally sophisticated families guided by independent, fee-only expertise, it also represents an opportunity to build truly antifragile portfolios.

Through exhaustive multidimensional diversification, meticulous jurisdictional layering, strategic private market allocation, advanced hedging, integrated family governance, and vigilant scenario-driven adaptation, capital can be positioned not merely to survive but to prosper amid uncertainty. The families that embrace this comprehensive resilience framework today will secure serenity, continuity, and enhanced growth for generations to come, transforming the very risks that unsettle others into the foundation of enduring legacy in an unpredictable world.