In the dynamic landscape of global equity markets, 2026 has begun with a fascinating interplay between persistent geopolitical uncertainties and the unwavering optimism fueling stock valuations. Despite intermittent volatility in the early weeks of the year, global stocks have advanced about 3% year-to-date, lingering near record highs. This resilience is underpinned by a supportive economic environment, including accommodative monetary policies from major central banks and robust corporate profitability. As the fourth-quarter earnings season unfolds, analyst consensus remains optimistic: global earnings growth is projected at approximately 15% for fiscal year 2026 and 14% for 2027, following a solid 10% expansion in 2025.

However, with revenue streams already accelerating and U.S. profit margins reaching unprecedented peaks, questions arise about the sustainability of these elevated earnings projections for 2026. In this comprehensive analysis from Vellum Finance, we delve deeply into U.S. earnings exceptionalism, trends in margin expansion, and the broadening of global earnings growth. These elements are critical for investors navigating 2026 stock market trends, corporate earnings forecasts, and portfolio optimization strategies. We’ll also explore broader global economic outlooks, the transformative impact of artificial intelligence (AI), potential risks from trade policies and tariffs, and emerging opportunities in international markets.

The global economic backdrop for 2026 appears steady, with projections from the International Monetary Fund (IMF) indicating growth of 3.3% for 2026, slightly up from previous estimates, driven by technology investments, fiscal support, and private sector adaptability. Similarly, Goldman Sachs Research anticipates a “sturdy” global growth rate of 2.8%, outperforming consensus forecasts, with the U.S. leading at 2.6% due to reduced tariff impacts and tax cuts. J.P. Morgan Global Research echoes this positivity, forecasting double-digit equity gains across developed and emerging markets, bolstered by AI advancements and lower interest rates. PwC’s outlook aligns, predicting 2.7% global GDP growth, with resilience amid uneven regional momentum.

This favorable environment sets the stage for continued equity market performance, but investors must remain vigilant. As we expand on these themes, we’ll incorporate insights from multiple sources to provide a balanced, multifaceted view, helping you refine your 2026 investment strategies for global stock market trends and corporate profitability.

U.S. Earnings Exceptionalism: The Engine of Global Stock Market Strength

The narrative of U.S. stock market underperformance in prior cycles often overlooks the underlying strength in corporate earnings. In 2025, U.S. firms delivered a remarkable 14% earnings growth based on fourth-quarter estimates, starkly contrasting with flat earnings in the UK and Europe for the second year running, further aggravated by currency headwinds such as a weakening dollar. This divergence has intensified since 2016, cementing U.S. earnings exceptionalism as a key driver of global market dynamics.

Over the past decade, U.S. companies have compounded earnings growth at 9%, surpassing continental Europe’s 5% and Asia’s 3%. This outperformance stems from sectoral advantages: The U.S. market’s heavy tilt toward high-growth technology sectors contrasts with Europe’s and Asia’s reliance on cyclical industries like banking and materials. China’s prolonged profit slump has further dragged down Asian aggregates.

Since mid-2018, when regional earnings trajectories began to diverge sharply, roughly one-third of U.S. earnings growth has been attributable to the ‘Magnificent Seven’, Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Excluding these tech behemoths, the remaining 493 S&P 500 constituents exhibit earnings growth only slightly ahead of Europe’s over the same timeframe. For investors eyeing 2026 stock market forecasts, grasping this tech-fueled U.S. dominance is essential for effective portfolio strategy and risk mitigation.

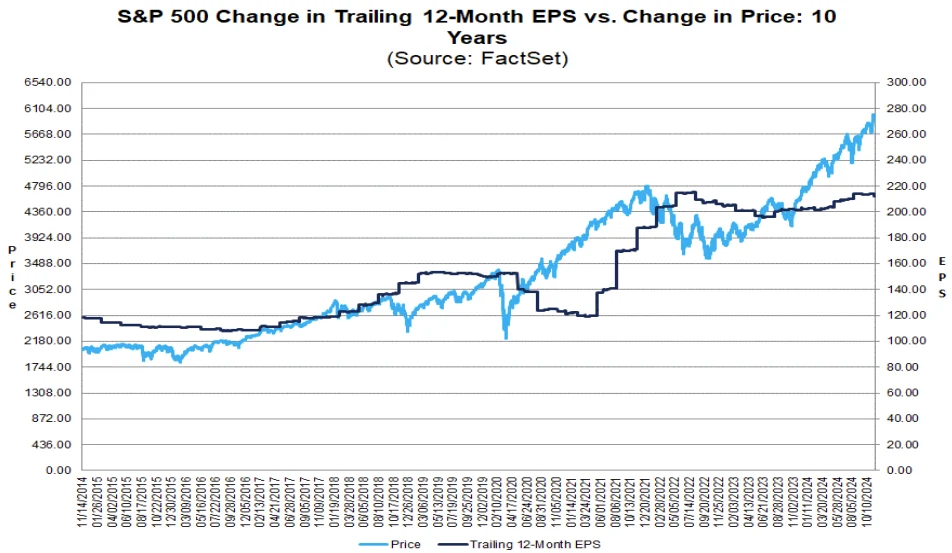

To illustrate this trend, consider the historical indexed earnings data:

Figure 1: Selected Trailing Earnings (EPS in USD, Indexed to 100 on January 31, 2016)

Is the S&P 500 overvalued? | MarketScreener

Source: Vellum Finance, MSCI, Bloomberg. Note: ‘Mag7’ includes Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Additional data from FactSet and Goldman Sachs Research highlights the Magnificent Seven’s projected 22.7% earnings growth for CY 2026, slightly above 2025’s 22.3%.

Expanding on this, the U.S. economy’s resilience, bolstered by fiscal stimuli like the One Big Beautiful Bill Act (OBBBA), has amplified this exceptionalism. Deloitte’s global economic outlook notes that U.S. real GDP growth is expected at 1.9% in 2026, with risks tilted downward, yet AI-related investments could provide upside. RSM economists forecast a rebound to 2.2% U.S. growth, driven by fiscal easing and deregulation.

Historically, U.S. earnings have benefited from globalization, tax reforms, and declining interest rates. However, as BlackRock’s Gargi Chaudhuri points out, 2026 could see earnings broadening amid volatility, with cyclical rotations favoring value over growth. iShares’ 2026 outlook emphasizes improving fundamentals beyond AI, with S&P 500 earnings per share growth accelerating to 12% in Q3 2025 ex-tech and comms.

This exceptionalism isn’t without challenges. Stifel’s 2026 outlook warns of AI as a double-edged sword: a driver of productivity but a risk if adoption slows. Bessemer Trust projects 14.3% S&P 500 earnings growth, supported by fiscal policy and broadening sectors. Yahoo Finance highlights Wall Street’s expectation of profit growth powering markets, with 8.3% Q4 2025 growth potentially rising to 14%.

Merrill Edge’s Savita Subramanian forecasts 15% profits growth, double the norm, but notes hot profits may temper market gains. In summary, U.S. earnings exceptionalism remains a cornerstone for 2026 global stock market trends, but diversification beyond tech is prudent.

Can U.S. Profit Margins Continue Expanding in 2026?

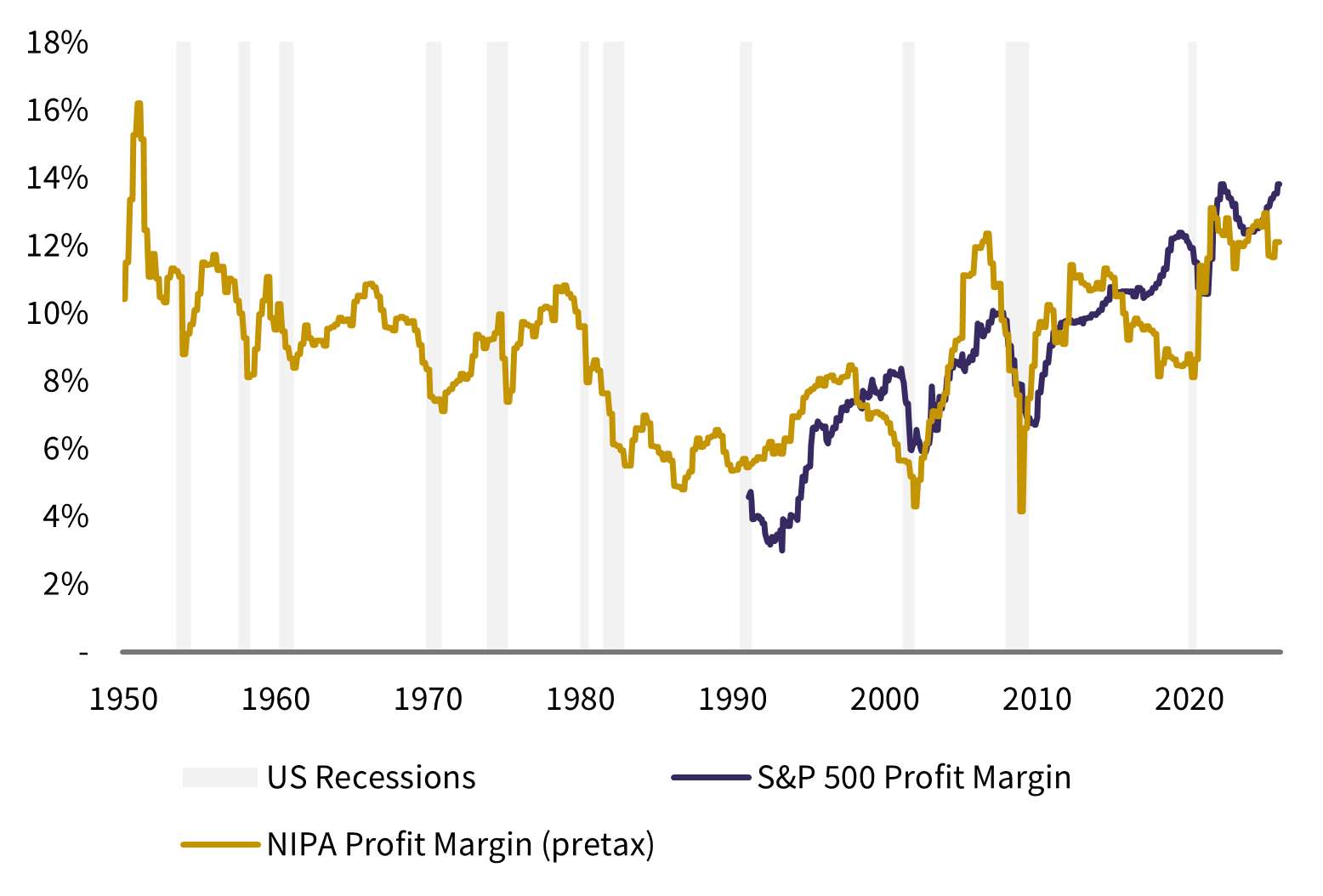

A pivotal force behind U.S., and especially tech-dominated, earnings has been sustained margin expansion over three decades. Current U.S. profit margins hover at about 14%, the highest in available bottom-up data.

This expansion ties to sectoral efficiencies: Technology’s scalability demands minimal capital outlay. Yet, most non-tech sectors (barring real estate and healthcare) have also enhanced profitability through globalization, reduced taxes, and historically low interest rates.

Skeptics advocate for mean reversion, citing risks like tariffs, high rates, or de-globalization. However, long-term national accounts data suggest pre-tax margins today align closer to historical norms than outliers.

Figure 2: S&P 500 Post-Tax (Bottom-Up) and NIPA Pre-Tax (Whole-Economy) Margins

Source: Vellum Finance, BEA, S&P Global, Bloomberg. Note: NIPA data from the U.S. Bureau of Economic Analysis reflects income from current production across all U.S. corporations, including private firms, on a consistent basis. S&P 500 data covers major public companies under GAAP accounting. BlackRock notes illustrative 4% margin increases could imply $878 billion in incremental profits.

For 2026, U.S. earnings hinge on further margin growth, which may face hurdles. AI models are capital- and energy-intensive, potentially straining resources. Without widespread AI productivity spillovers, promising long-term but uncertain short-term, disappointments could arise.

Stanford’s SIEPR highlights 2026 focuses: Fed rates, job markets, AI valuations, affordability, and fiscal constraints. Roosevelt Institute predicts a “meh” year post-2025 stagflation, with inflation at 2.8%. Ameriprise forecasts 2.5% GDP growth, with AI shifting from hype to proof.

Mercer expects accommodative policy, with Fed rates below 3% by year-end. Yahoo Finance notes expanding margins across sectors, with 14% earnings growth. Silvercrest sees equities compelling over three years, powered by margin boosts from AI.

RSM warns of “stagflation lite,” with 2.7% PCE inflation. Reuters reports Builders FirstSource forecasting 28.5%-30% margins, below estimates. Crossmark and Apollon highlight healthy margins, with small caps improving to 5%.

Sherwood News dubs 2026 a “golden age” with 13.9% margins. Bloomberg compiles forecasts, with nominal GDP north of 5%. For “U.S. profit margins 2026” seekers, Vellum Finance advises close monitoring for optimal decisions.

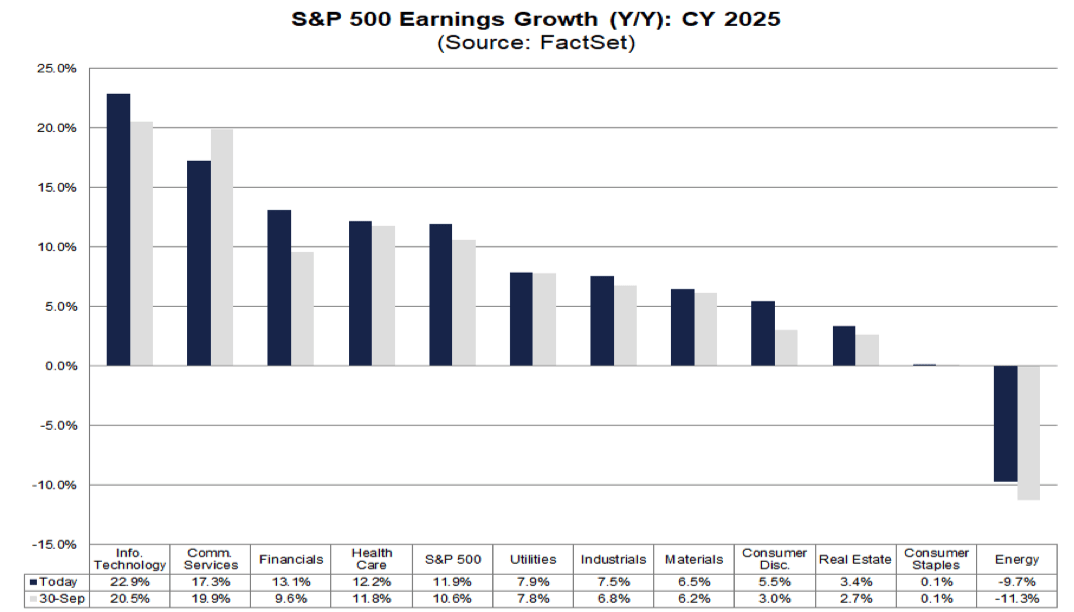

Broadening Earnings Growth: Opportunities Beyond Tech in Global Markets

While technology leads 2026 earnings, the outlook balances across sectors. Energy, contracting for three years, is poised to rebound amid reflationary trends.

Financials may gain from U.S. deregulation, steeper yield curves, and low impairments. Materials could benefit from AI infrastructure and metal scarcities.

This broadening extends regionally, with Europe, UK, and emerging Asia forecasting double-digit growth.

Figure 3: Developed Market Sector Earnings Growth

| Sector | FY 2025 EPS Growth | FY 2026 EPS Growth | FY 2027 EPS Growth |

| Technology | 22.9% | 18.4% | 15.2% |

| Energy | -9.7% | 7.5% | 6.8% |

| Financials | 13.1% | 12.6% | 11.4% |

| Industrials | 7.5% | 10.5% | 9.8% |

| Materials | 6.5% | 9.2% | 8.7% |

| Health Care | 12.2% | 11.8% | 10.9% |

| Utilities | 7.9% | 8.5% | 7.6% |

| Consumer Disc. | 5.5% | 7.4% | 6.9% |

| Real Estate | 3.4% | 5.6% | 5.1% |

| Consumer Staples | 0.1% | 4.2% | 3.8% |

Source: Vellum Finance, Bloomberg, MSCI. Expanded with data from Schwab, noting AI favoring hyperscalers.

Source: Vellum Finance, Bloomberg, MSCI. Expanded with data from Schwab, noting AI favoring hyperscalers.

J.P. Morgan sees EM equities boosted by lower rates and governance improvements. BNY notes broadening earnings beyond big tech. Morgan Stanley warns of razor-thin margins for non-Mag7.

Mercer highlights AI-driven growth but elevated valuations. FactSet predicts 15% S&P growth, with all sectors positive. iShares notes Q3 2025 broadening.

Investing.com observes value outperforming growth. Fidelity identifies power demand and GLP-1 effects as themes. State Street emphasizes relative earnings for allocation.

Macro Moments forecasts 16% EM EPS growth. Bessemer sees industrials leading. Goldman projects 11% global returns. Yahoo notes cyclical tilt. Coutts highlights EM diversification.

Geopolitical hurdles persist, but strengthening economies could sustain momentum. For “global earnings growth 2026,” these trends are pivotal for diversification.

Global Economic Outlook: Navigating Growth Amid Uncertainties

Beyond U.S.-centric views, the global economy in 2026 is projected to maintain resilience. IMF’s update sees 3.3% growth, offsetting trade shifts. Goldman anticipates 2.8%, with U.S. outperformance.

J.P. Morgan notes 35% recession probability but resilient growth. PwC forecasts 2.7%, with U.S. at 2.1% and India at 6.7%. TD sees 8-12% U.S. equity returns, with broadening.

FactSet expects 15% S&P growth. Hartford Funds highlights AI supporting equities. BNY notes cyclical rotations.

Mercer sees steady growth led by U.S. Deloitte details regional variations, with China at 4.5%. RSM predicts 2.2% U.S. growth.

This outlook supports buoyant earnings but underscores risks like tariffs.

The Transformative Impact of AI on 2026 Earnings

Artificial intelligence (AI) remains one of the most dominant megatrends in 2026, profoundly influencing corporate profitability, productivity, and global equity markets. Often described as an AI supercycle, this wave of innovation continues to drive above-trend earnings growth across major indices, particularly in technology and infrastructure-related sectors.

J.P. Morgan Global Research emphasizes the AI supercycle as a primary driver of sustained economic momentum, projecting S&P 500 earnings growth of 13% to 15% over the next two years. This optimism stems from record levels of capital expenditure (capex), accelerating adoption rates, and emerging productivity gains. Hyperscalers, leading cloud and AI infrastructure providers like Alphabet, Amazon, Meta, Microsoft, Oracle, and Nvidia, have dramatically ramped up spending. Annual capex from these large U.S. tech companies has tripled from $150 billion in 2023 to potentially over $500 billion in 2026, with these firms now accounting for nearly 25% of total U.S. market capex. In fact, AI-related investment contributed more to U.S. GDP growth than consumer spending in 2025, and this impulse is expected to persist strongly into 2026, fueling demand for inference (real-world AI model deployment) and broader enterprise adoption.

BlackRock’s Investment Institute views AI as a central, long-term theme, anticipating another $5–8 trillion in related capex through 2030. The firm notes that much of 2025’s tech rally was powered by robust earnings growth rather than valuation expansion, with multiples even contracting slightly while remaining justified by underlying growth prospects. BlackRock frames AI primarily as a cost and margin enhancer, delivering productivity lifts, higher returns on equity for efficient adopters, and a potential 1.5% structural boost to U.S. growth through widespread implementation, equating to roughly $1.1 trillion in expanded economy-wide revenues. As AI adoption extends beyond infrastructure builders into utilities, industrials, materials, and other sectors, it could create sustained demand for power and efficiency improvements, although this will strain clean energy infrastructure and grids.

Goldman Sachs Research highlights massive AI-related spending, with consensus estimates for infrastructure companies now reaching $527 billion in 2026 capex (up from $465 billion earlier in the earnings cycle). This supports robust demand for semiconductors, networking, data centers, and cloud services, projecting technology sector earnings growth of around 26% and semiconductors near 50%. However, challenges persist, including risks of overcapacity, commoditization of certain components, and uncertainty around near-term monetization. Big Tech’s projected $530–650 billion (or higher) infrastructure spend in 2026 raises scrutiny on translating these investments into sustainable revenue streams and margins, with investor focus intensifying on measurable returns.

Stanford’s Institute for Economic Policy Research (SIEPR) examines AI valuations, pointing to potentially bubbly characteristics where AI-exposed stocks have risen sharply despite limited immediate revenue from AI-specific offerings. Yet, if generative AI unlocks substantial labor productivity gains, potentially adding trillions in value for U.S. firms, current valuations may appear conservative. SIEPR anticipates 2026 as a pivotal shift from hype to tangible utility, with no arrival of artificial general intelligence (AGI) but greater emphasis on real ROI, domain-specific performance, and measurable outcomes such as accuracy, efficiency, and cost savings across industries from legal services to enterprise operations.

PwC’s 2026 AI Business Predictions underscore that while only a handful of companies currently capture extraordinary value, evidenced by surging top-line growth and valuation premiums, the landscape is evolving toward more focused strategies, agentic workflows (autonomous AI agents), and responsible innovation frameworks that deliver transformative business impact. McKinsey estimates generative AI could contribute up to $4.4 trillion annually to the global economy through enhanced productivity, cost reductions, and new revenue opportunities, with global AI spending projected to approach $2 trillion in 2026.

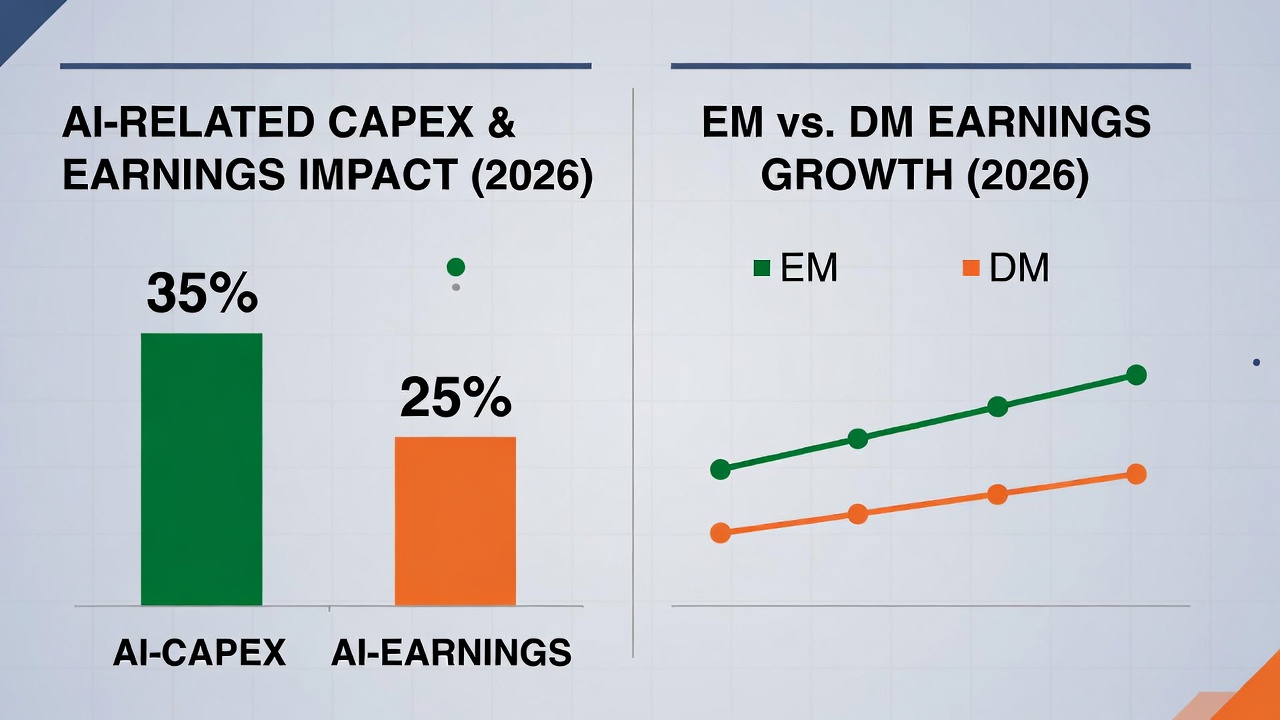

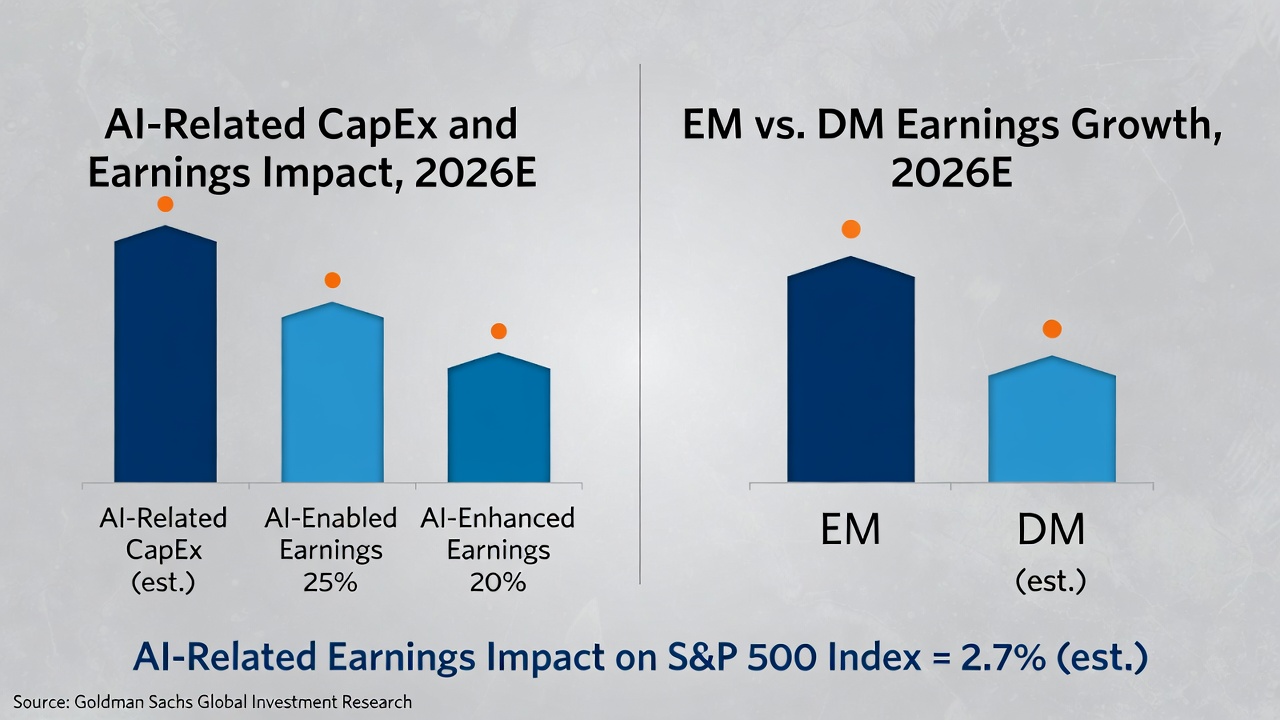

Figure 4: Projected AI-Related Capex and Earnings Impact (2026 Estimates)

Source: Compiled from J.P. Morgan, Goldman Sachs, BlackRock, PwC, and consensus analyst data. Note: Capex figures reflect updated consensus for hyperscalers and infrastructure providers (potentially $500–700 billion aggregate); earnings growth linked to phased AI adoption, with tech/semiconductors leading.

Source: Compiled from J.P. Morgan, Goldman Sachs, BlackRock, PwC, and consensus analyst data. Note: Capex figures reflect updated consensus for hyperscalers and infrastructure providers (potentially $500–700 billion aggregate); earnings growth linked to phased AI adoption, with tech/semiconductors leading.

AI holds significant potential to boost corporate margins through scalability, automation, and operational efficiencies. Fidelity highlights that AI investments are largely funded by high free cash flows among leading firms, enabling mid-20% earnings growth for key cohorts compared to flat or single-digit growth for the broader S&P 500. However, risks remain prominent: overcapacity in energy-intensive models, uneven spillover of productivity benefits beyond early adopters, and potential valuation bubbles if monetization timelines extend longer than anticipated. Overall, AI’s transformative role, spanning inference monetization, agentic systems, sector-wide efficiency gains, and infrastructure expansion, positions it as a core driver of 2026 earnings momentum, though realization depends on disciplined execution, measurable ROI, and continued broadening adoption across the economy.

Risks: Tariffs, Geopolitics, and Policy Shifts

Tariffs continue to pose meaningful downside risks to 2026 earnings and broader growth trajectories. Deloitte’s U.S. Economic Forecast incorporates assumptions of modestly elevated tariffs persisting, with the average effective rate potentially reaching 15% by Q1 2026 and holding through 2030. This could generate substantial revenue (around $2.5 trillion over the decade) but would pressure consumption, business investment, and import volumes.

The Congressional Budget Office (CBO) projects that higher tariffs would reduce real GDP relative to a baseline scenario without them, while temporarily elevating inflation, diminishing purchasing power, and constraining investment, though partially mitigated by fiscal support measures. In its Budget and Economic Outlook for 2026–2036, the CBO notes tariffs could increase customs duties from 0.6% to 1.3% of GDP in 2026 before tapering, aiding deficit reduction by about $3 trillion through 2035 (including dynamic effects) but restraining overall growth via elevated prices and supply chain frictions.

Geopolitical tensions, from trade barriers and fragmentation to regional conflicts, add layers of volatility. Nevertheless, resilient fundamentals such as AI-driven productivity enhancements and steady consumer demand may help offset contained risks, supporting earnings resilience in a challenging macro environment.

Emerging Opportunities in International Markets

While U.S. markets benefit heavily from AI leadership, international and emerging markets (EM) present compelling broadening opportunities in 2026. Morgan Stanley’s Investment Outlook identifies key themes including Tech Diffusion (global AI spread), The Future of Energy, The Multipolar World, and Societal Shifts, which position EM for gains through supply chain realignments, policy reforms, and diversification.

Goldman Sachs Research forecasts global growth at a sturdy 2.8% in 2026 (above consensus 2.5%), with global equities expected to deliver 11% total returns over the next 12 months (including dividends, in USD), primarily earnings-driven rather than valuation-led. EM and Asia are highlighted for strong long-term local-currency returns.

Franklin Templeton remains constructive on EM equities, citing sustained momentum from AI-related investments (e.g., semiconductor supply chains and digitalization), policy enhancements in China, Korea, and India, premiumization trends in consumption and healthcare, and attractive relative valuations versus developed markets. Combined with growth-supportive policies, EM earnings momentum could fuel outperformance, offering selective opportunities across debt, sovereigns, and corporates amid solid fundamentals and evolving geopolitical dynamics.

S&P Global anticipates EM outperformance potential, while Vanguard cautions on persistent inflation risks and Schwab highlights international strength. The Globe and Mail points to UK market bargains, McKinsey notes a private equity rebound, and Franklin Templeton stresses EM’s leadership role in a broadening bull market.

Figure 5: EM vs. Developed Markets Earnings Growth Outlook (2026 Projections)

Source: Aggregated from Franklin Templeton, Goldman Sachs, Morgan Stanley, and consensus insights. Note: EM benefits from AI supply chain participation, structural reforms, and valuation discounts relative to developed markets.

Source: Aggregated from Franklin Templeton, Goldman Sachs, Morgan Stanley, and consensus insights. Note: EM benefits from AI supply chain participation, structural reforms, and valuation discounts relative to developed markets.

These dynamics reinforce the value of diversification beyond U.S. tech dominance, with EM positioned for earnings-led gains supported by macro tailwinds and thematic alignment.

Unlock Your Investment Potential with Vellum Finance

At Vellum Finance, we provide actionable, data-driven insights into 2026 earnings forecasts, global stock market trends, corporate profitability drivers, AI’s transformative effects, tariff-related risks, and international diversification opportunities. Our tailored strategies balance U.S. exceptionalism with EM broadening to build resilient, growth-oriented portfolios. Contact a Vellum Finance Advisor today for personalized 2026 investment guidance aligned with your objectives and risk profile.

Past performance is not indicative of future results. This article does not constitute financial advice. Information from reliable sources, but no warranties on accuracy. Opinions subject to change.